National Real Estate Market Update for 2023

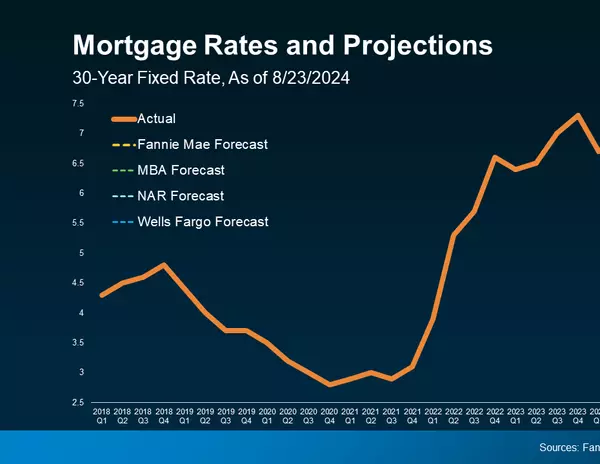

There’s an old adage in real estate: location, location, location. But ever since the Federal Reserve began its series of inflation-fighting interest rate hikes last year, a new mantra has emerged: mortgage rates, mortgage rates, mortgage rates. Higher rates had the immediate impact of dampening homebuyer affordability and demand. But this year, we’re seeing further repercussions. While analysts expected listing inventory to swell as sales declined, instead, homeowners have been pushing off plans to sell because they feel beholden to their existing, lower mortgage rates. So what impact is this reduced demand and low supply environment having on home values? And what can we expect from the real estate market in the coming months and years? Here are several key indicators that help to paint a picture of the current market and where it’s likely headed. HOME SALES ARE EXPECTED TO PICK UP BY EARLY NEXT YEAR The weather isn’t the only thing that heats up in the spring and summer. Nationally, it tends to be the busiest time in real estate. But this year, the peak season got off to a slow start, with sales declines in both March and April.1,2 Existing home sales in April were down 3.4% from the previous month—and 23.2% from a year earlier.2 What’s causing this market slowdown? Industry experts attribute it to several factors, including near-record home prices, high mortgage rates, and low inventory. According to National Association of Realtors (NAR) Chief Economist Lawrence Yun, “Home sales are trying to recover and are highly sensitive to changes in mortgage rates. Yet, at the same time, multiple offers on starter homes are quite common, implying more supply is needed to fully satisfy demand. It's a unique housing market.”1 However, some industry experts believe the market is poised for a comeback. Forecasters at the Mortgage Bankers Association (MBA) predict that home sales will continue to fall through Q3 before rising in Q4 and throughout next year.3 Analysts at Fannie Mae expect the recovery to take a bit longer, picking up in early 2024. Meanwhile, home builder confidence is already up, as purchases of new single-family homes surged in March and April to a 13-month high.5 Builder incentives are helping to boost sales: According to the National Association of Home Builders, in May, 54% reported using them to win over budget-conscious buyers.6 What does it mean for you? A slower pace of sales has given buyers some breathing room. If you hated the frenzy of the pandemic-era real estate market, now might be a better time for you to shop for a home. We can help you evaluate your options and make an informed purchase. If you plan to sell your home, prepare yourself for less foot traffic and a longer sales timeline than you may have found a year ago. It will also be crucial to enlist the help of a skilled agent who knows how to draw in buyers. Reach out for a copy of our multi-step Property Marketing Plan. PROPERTY VALUES REMAIN RELATIVELY STABLE Some good news for buyers: While home builder sales climbed in April, the median new-house price fell to $420,800, an 8.2% decrease from a year ago.5 Meanwhile, the median existing-home price dropped to $388,800, down 1.7% year-over-year. Notably, existing-home prices rose in parts of the country but fell in the South and West.2 “Roughly half of the country is experiencing price gains,” explains Yun. “Multiple-offer situations have returned in the spring buying season following the calmer winter market. Distressed and forced property sales are virtually nonexistent.”2 The average national home price remains about 40% higher than it was in early 2020, according to the S&P CoreLogic Case-Shiller index.7 A tight housing supply has helped to buoy prices amidst a slowdown in sales. “While it varies from region to region, home prices at the national level may fall 1% or 1.5% by the end of the year, so not much,” Doug Duncan, senior vice president and chief economist at Fannie Mae, told Yahoo Finance in April.8 Record levels of home equity will help to stabilize the sector and prevent a wave of foreclosures, even as prices moderate, according to Mark Zandi, chief economist at Moody’s Analytics.9 “But for those who have owned a home for more than a year or two, their home will remain a rock-solid investment. And once affordability is restored, the next generation of households can become homeowners. Getting there is critical to the financial well-being of those households, their communities, and the broader economy,” writes Zandi in The Washington Post.9 What does it mean for you? Prices have softened in certain market segments—and motivated sellers are out there and willing to make deals. We can help you find your next home and negotiate a great price. If you’re a homeowner, the surge in home values has slowed, but you’re likely still sitting on a nice pile of equity. Reach out for a free assessment to find out how much your home is currently worth. LISTING INVENTORY IS LOW, BUT NEW CONSTRUCTION IS ON THE RISE Unsold existing home inventory rose 7.2% from March to April, according to NAR. At the current level of demand, this equates to 2.9 months of supply, which is still well below the 5 to 6 months of inventory required for a “balanced” market.2 Inventory remains tight despite the market slowdown because many would-be sellers are reluctant to give up their lower mortgage rates. “Affordability is not only an issue for first-time homebuyers, but also for many repeat buyers who still need to take on a mortgage,” explains Danielle Hale, chief economist for Realtor.com.10 In a recent survey by the home listing site, 82% of respondents who are planning to both buy and sell a home said they feel “locked in” by their low rate.11 In some areas, new home construction is helping to fill the supply gap. “Currently, one-third of housing inventory is new construction, compared to historical norms of a little more than 10%,” according to National Association of Home Builders Chief Economist Robert Dietz.12 And more new homes are in the pipeline, after a builder slowdown last year. Single-family housing starts rose 1.6% from March to April (seasonally adjusted) and new construction permits hit a seven-month high.13 What does it mean for you? Inventory remains tight, but less competition means more choice and negotiating power for buyers. If you’ve had trouble finding a home in the past, it may be time to take another look. We can help you explore both new and existing homes in our area. Sellers are enjoying reduced competition right now, as well. However, the longer you wait to list, the more competition you’re likely to face. And if you feel locked in by your current, lower mortgage rate, consider this: If you roll your equity gains into a down payment on your next home, you could possibly lower your monthly payment. Reach out to discuss your options. MORTGAGE RATES MAY FINALLY COME DOWN According to Freddie Mac, the average 30-year fixed-rate mortgage hit a peak of 7.08% in the fourth quarter of 2022, and since then it’s primarily floated between 6 and 7%.14 However, there are signs that rates could trend lower later this year. “Calmer inflation means lower mortgage rates, eventually,” Yun predicted in a recent statement. “Mortgage rates slipping down to under 6% looks very likely toward the year’s end.”15 Other leading economists agree. In its May forecast, Fannie Mae speculates that 30-year fixed mortgage rates will continue to decline, averaging 6.0% in Q4 2023 and 5.4% by Q4 2024.4 Meanwhile, the MBA predicts rates will fall even faster, averaging 5.6% by Q4 2023 and 4.8% by Q4 2024.3 On May 3, the Federal Reserve raised its benchmark borrowing rate by another quarter point—its 10th consecutive increase since March 2022. However, in its corresponding statement, the Fed omitted language from its previous release about “additional policy firming,” leaving many analysts to speculate that the rate hikes may be over.16 Although mortgage rates aren’t directly tied to the federal funds rate, a decision by the Fed to pause rate increases could have a positive effect. In the meantime, buyers should shop around multiple lenders to find the best rate—and buckle up for what could be an exciting ride. What does it mean for you? Mortgage rates may finally trend down, which would be great news for buyers. But, a decrease in rates could correspond with an increase in competition and prices. If you start searching now, you’ll be prepared to make an offer when the time is right. We can help you negotiate a great deal and potential seller incentives. If you’re planning to sell, this is good news for you, too. But, there are several factors to consider when determining the right time to list your home. Reach out for a consultation so we can help you chart the best course. WE’RE HERE TO GUIDE YOU While national real estate forecasts can provide a “big picture” outlook, real estate is local. And as local market experts, we can guide you through the ins and outs of our market and the issues most likely to impact sales and drive home values in your particular neighborhood. If you’re considering buying or selling a home, contact us now to schedule a free consultation. We’ll work with you to develop an action plan to meet your real estate goals. The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate professionals for advice regarding your individual needs. Sources: National Association of Realtors -https://www.nar.realtor/newsroom/existing-home-sales-slid-2-4-in-march National Association of Realtors -https://www.nar.realtor/newsroom/existing-home-sales-faded-3-4-in-april Mortgage Bankers Association -https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/2023/mortgage-finance-forecast-may-2023.pdf?sfvrsn=4bf1d1a7_1 Fannie Mae -https://www.fanniemae.com/media/47006/display U.S. Census Bureau -https://www.census.gov/construction/nrs/current/index.html National Association of Home Builders -https://www.nahb.org/news-and-economics/press-releases/2023/05/lack-of-existing-inventory--boosts-builder-confidence-to-key-marker New York Times -https://www.nytimes.com/2023/04/29/business/spring-housing-market.html? Yahoo Finance -https://finance.yahoo.com/news/mortgage-rates-increase-after-weeks-of-declines-160015631.html The Washington Post -https://www.washingtonpost.com/business/2023/04/22/housing-prices-put-some-out-of-the-market/ CNBC -https://www.cnbc.com/2023/04/20/home-sales-fell-in-march-amid-volatility-in-mortgage-rates.html Realtor.com -https://www.realtor.com/research/2023-q1-sellers-survey-btts/ National Association of Home Builders -https://www.nahb.org/news-and-economics/press-releases/2023/04/lack-of-existing-inventory-continues-to-support-builder-sentiment United State Census Bureau -https://www.census.gov/construction/nrc/pdf/newresconst.pdf Freddie Mac -https://www.freddiemac.com/pmms National Association of Realtors -https://www.nar.realtor/blogs/economists-outlook/instant-reaction-inflation-april-12-2023 CNBC -https://www.cnbc.com/2023/05/03/fed-rate-decision-may-2023-.html

Take Advantage of Your Home Equity: A Homeowner’s Guide

Homeownership offers many advantages over renting, including a stable living environment, predictable monthly payments, and the freedom to make modifications. Neighborhoods with high rates of homeownership have less crime and more civic engagement. Additionally, studies show that homeowners are happier and healthier than renters, and their children do better in school.1 But one of the biggest perks of homeownership is the opportunity to build wealth over time. Researchers at the Urban Institute found that homeownership is financially beneficial for most families,2 and a recent study showed that the median net worth of homeowners can be up to 80 times greater than that of renters in some areas.3 So how does purchasing a home help you build wealth? And what steps should you take to maximize the potential of your investment? Find out how to harness the power of home equity for a secure financial future. WHAT IS HOME EQUITY? Home equity is the difference between what your home is worth and the amount you owe on your mortgage. So, for example, if your home would currently sell for $850,000, and the remaining balance on your mortgage is $400,000, then you have $450,000 in home equity. $850,000 (Home’s Market Value) - $400,000 (Mortgage Balance) ______________________________ $450,000 (Home Equity) The equity in your home is considered a non-liquid asset. It’s your money; but rather than sitting in a bank account, it’s providing you with a place to live. And when you factor in the potential of appreciation, an investment in real estate will likely offer a better return than any savings account available today. HOW DOES HOME EQUITY BUILD WEALTH? A mortgage payment is a type of “forced savings” for home buyers. When you make a mortgage payment each month, a portion of the money goes towards interest on your loan, and the remaining part goes towards paying off your principal, or loan balance. That means the amount of money you owe the bank is reduced every month. As your loan balance goes down, your home equity goes up. Additionally, unlike other assets that you borrow money to purchase, the value of your home generally increases, or appreciates, over time. For example, when you pay off your car loan after five or seven years, you will own it outright. But if you try to sell it, the car will be worth much less than when you bought it. However, when you purchase a home, its value typically rises over time. So when you sell it, not only will you have grown your equity through your monthly mortgage payments, but in most cases, your home’s market value will be higher than what you originally paid. And even if you only put down 10% at the time of purchase—or pay off just a small portion of your mortgage—you get to keep 100% of the property’s appreciated value. That’s the wealth-building power of real estate.WHAT CAN I DO TO GROW MY HOME’S EQUITY FASTER? Now that you understand the benefits of building equity, you may wonder how you can speed up your rate of growth. There are two basic ways to increase the equity in your home: 1. Pay down your mortgage.We shared earlier that your home’s equity goes up as your mortgage balance goes down. So paying down your mortgage is one way to increase the equity in your home. Some homeowners do this by adding a little extra to their payment each month, making one additional mortgage payment per year, or making a lump-sum payment when extra money becomes available—like an annual bonus, gift, or inheritance. Before making any extra payments, however, be sure to check with your mortgage lender about the specific terms of your loan. Some mortgages have prepayment penalties. And it’s important to ensure that if you do make additional payments, the money will be applied to your loan principal. Another option to pay off your mortgage faster is to decrease your amortization period. For example, if you can afford the larger monthly payments, you might consider refinancing from a 30-year or 25-year mortgage to a 15-year mortgage. Not only will you grow your home equity faster, but you could also save a bundle in interest over the life of your loan.2. Raise your home’s market value. Boosting the market value of your property is another way to grow your home equity. While many factors that contribute to your property’s appreciation are out of your control (e.g. demographic trends or the strength of the economy) there are things you can do to increase what it’s worth. For example, many homeowners enjoy do-it-yourself projects that can add value at a relatively low cost. Others choose to invest in larger, strategic upgrades. Keep in mind, you won’t necessarily get back every dollar you invest in your home. In fact, according to Remodeling Magazine’s latest Cost vs. Value Report, the remodeling project with the highest return on investment is a garage door replacement, which costs about $3600 and is expected to recoup 97.5% at resale. In contrast, an upscale kitchen remodel—which can cost around $130,000—averages less than a 60% return on investment.4 Of course, keeping up with routine maintenance is the most important thing you can do to protect your property’s value. Neglecting to maintain your home’s structure and systems could have a negative impact on its value—therefore reducing your home equity. So be sure to stay on top of recommended maintenance and repairs. HOW DO I ACCESS MY HOME EQUITY IF I NEED IT? When you put your money into a checking or savings account, it’s easy to make a withdrawal when needed. However, tapping into your home equity is a little more complicated. The primary way homeowners access their equity is by selling their home. Many sellers will use their equity as a downpayment on a new home. Or some homeowners may choose to downsize and use the equity to supplement their income or retirement savings. But what if you want to access the equity in your home while you’re still living in it? Maybe you want to finance a home renovation, consolidate debt, or pay for college. To do that, you will need to take out a loan using your home equity as collateral. There are several ways to borrow against your home equity, depending on your needs and qualifications:5 Second Mortgage - A second mortgage, also known as a home equity loan, is structured similarly to a primary mortgage. You borrow a lump-sum amount, which you are responsible for paying back—with interest—over a set period of time. Most second mortgages have a fixed interest rate and provide the borrower with a predictable monthly payment. Keep in mind, if you take out a home equity loan, you will be making monthly payments on both your primary and secondary mortgages, so budget accordingly. Cash-Out Refinance - With a cash-out refinance, you refinance your primary mortgage for a higher amount than you currently owe. Then you pay off your original mortgage and keep the difference as cash. This option may be preferable to a second mortgage if you have a high-interest rate on your current mortgage or prefer to make just one payment per month. Home Equity Line of Credit (HELOC) - A home equity line of credit, or HELOC, is a revolving line of credit, similar to a credit card. It allows you to draw out money as you need it instead of taking out a lump sum all at once. A HELOC may come with a checkbook or debit card to enable easy access to funds. You will only need to make payments on the amount of money that has been drawn. Similar to a credit card, the interest rate on a HELOC is variable, so your payment each month could change depending on how much you borrow and how interest rates fluctuate. Reverse Mortgage - A reverse mortgage enables qualifying seniors to borrow against the equity in their home to supplement their retirement funds. In most cases, the loan (plus interest) doesn’t need to be repaid until the homeowners sell, move, or are deceased.6 Tapping into your home equity may be a good option for some homeowners, but it’s important to do your research first. In some cases, another type of loan or financing method may offer a lower interest rate or better terms to fit your needs. And it’s important to remember that defaulting on a home equity loan could result in foreclosure. Ask us for a referral to a lender or financial adviser to find out if a home equity loan is right for you. WE’RE HERE TO HELP YOU Wherever you are in the equity-growing process, we can help. We work with buyers to find the perfect home to begin their wealth-building journey. We also offer free assistance to existing homeowners who want to know their home’s current market value to refinance or secure a home equity loan. And when you’re ready to sell, we can help you get top dollar to maximize your equity stake. Contact us today to schedule a complimentary consultation! *The above references an opinion and is for informational purposes only. It is not intended to be financial advice. Consult a financial professional for advice regarding your individual needs. Sources: National Association of Realtors -https://www.nar.realtor/blogs/economists-outlook/highlights-from-social-benefits-of-homeownership-and-stable-housing Urban Institute - https://www.urban.org/urban-wire/homeownership-still-financially-better-renting Census Bureau -https://www.census.gov/library/stories/2019/08/gaps-in-wealth-americans-by-household-type.html Remodeling Magazine -https://www.remodeling.hw.net/cost-vs-value/2019/ Investopedia -https://www.investopedia.com/mortgage/heloc/home-equity/ Bankrate -https://www.bankrate.com/mortgage/reverse-mortgage-guide/

Why Real Estate Investing Makes (Dollars and) Sense

INTRODUCTION Turn on the television or scroll through Facebook, and chances are you’ll see at least one advertisement for a group or “guru” who promises to teach you how to “get rich quick” through real estate investing. The truth is, much of what they’re selling are high-risk tactics that aren’t a good fit for the average investor. However, there is a way to make steady, predictable, low-risk income through real estate investing. In this blog post, we’ll examine the tried-and-true tactics that can be used to increase your income, pay off debt … even fund your retirement! WHY INVEST IN REAL ESTATE? One of the basic principles of real estate investment lies in this fact: everyone needs a place to live. And according to the Bureau of Labor Statistics’ most recent Consumer Expenditures Survey, housing is typically an American’s largest expense.1 But there are other reasons why real estate is a great investment choice, and we’ve outlined the top five below: 1. Appreciation Appreciation is the increase in your property’s value over time. History has proven that over an extended period of time, the value of real estate continues to rise. That doesn’t mean recessions won’t occur. The real estate market is cyclical, and market ups and downs are natural. In fact, the U.S. housing market took a sharp downturn in 2008, and many properties took several years to recover their value. However, in the vast majority of markets, the value of real estate does grow over the long term. The S&P CoreLogic Case-Shiller National Home Price Index, which tracks U.S. residential real estate prices, released its latest results on August 29 with the headline “National Home Price Index Rises Again to All Time High.”2 While no investment is without risk, real estate has proven again and again to be a solid choice to invest your money over the long term. 2. Hedge Against Inflation Inflation is the rate at which the general cost of goods and services rises. As inflation rises, prices go up. This means the money you have in your bank account is essentially worth less because your purchasing power has decreased. Luckily, real estate prices also rise when inflation increases. That means any money you have invested in real estate will rise with (or often exceed) the rate of inflation. Therefore, real estate is a smart place to put your money to guard against inflation. 3. Cash Flow One of the big benefits of investing in real estate over the stock market is its ability to provide a fairly steady and predictable monthly cash flow. That is, if you choose to rent out your investment property to a tenant, you can expect to receive a rent payment each month. If you’ve invested wisely, the rent payment should cover the debt obligation you may have on the property (i.e. mortgage), as well as any repairs and maintenance that are needed. Ideally, the monthly rental income would be great enough to leave you a little extra cash each month, as well. You could use that extra money to pay off the mortgage faster, cover your own household expenses, or save for another investment property. Even if you only take in enough rent to cover your expenses, a rental property purchase will pay for itself over time. As you pay down the mortgage every month with your rental income, your equity will continue to increase, until you own the property free and clear … leaving you with residual cash flow for years to come. As the owner, you will also benefit from the property’s appreciation when it comes time to sell. This can be a great way to save for retirement or even fund a child’s college education. Purchase a property when the child is young, and with a little discipline, it can be paid off by the time they are ready to go to college. You can sell it for a lump sum, or use the monthly income to pay their tuition and expenses. 4. Leverage One of the unique features that sets real estate apart from other asset classes is the ability to leverage your investment. Leverage is the use of borrowed capital to increase the potential return on investment. For example, if you purchase an investment property for $100,000, you might put 10% down ($10,000) and borrow the remaining $90,000 in the form of a mortgage. Even though you’ve only invested $10,000 at this point, you have the ability to earn a profit on the entire $100,000 investment. So, if the property appreciates to $120,000 – a 20% increase over the purchase price – you still only have to pay the bank back the original $90,000 (plus interest) … and you get to keep the $20,000 profit. That means you made $20,000 off of a $10,000 investment, essentially doubling your money, even though the market only went up by 20%! That’s the power of leverage. 5. Tax Advantages One of the top reasons to invest in real estate is the tax benefit. There are numerous ways a real estate investment can save you money each year on taxes: Depreciation When you record your income from a rental property on your annual tax return, you get to deduct any expenses associated with the investment. This includes interest paid on the mortgage, maintenance, repairs and improvements, but it also includes something called depreciation. Depreciation is the theoretical loss your property suffers each year due to aging. While it’s true that as a home ages it will structurally need repairs and systems will eventually need to be replaced, we’ve also learned in this post that the value of real estate appreciates over time. So getting to claim a “loss” on your investment that is actually gaining in value makes real estate an appealing investment choice. Serial Home Selling Even if you’re not interested in owning a rental property, other types of real estate investments offer tax advantages, as well. Generally, when you own an investment property you pay a capital gains tax on any profits you make when you sell the property. However, when you sell your principal residence, you are exempt from paying taxes on capital gains (up to $250,000 for singles and $500,000 for couples). The Internal Revenue Service (IRS) only requires that you live in the house for two of the previous five years. That means you can purchase an investment property, live in it while you remodel it, and then sell it for a tax-free profit two years later. This can be a great way to get started in real estate investing. Section 1031 Exchanges In addition to profiting off of your personal residence tax free, it is possible to sell an investment property tax free if you do it through a 1031 Exchange. If structured properly, the IRS Tax Code enables an investor to sell a property and reinvest the proceeds in a new property while deferring all capital gains taxes. Tax-Deferred Retirement Account It’s a common misconception that you can only purchase financial instruments (i.e. stocks, bonds, mutual funds, etc.) through an Individual Retirement Account (IRA) or 401(k). In actuality, the IRS allows individuals to invest retirement funds in real estate and other alternative types of investments, as well. By purchasing your investment property through an IRA, you can take advantage of all of the tax savings these accounts offer. Be sure to consult a tax professional regarding all tax matters related to your real estate investments. If structured correctly, the profits you earn on your real estate investments can be largely shielded from tax liability. Just another reason to choose real estate as your preferred investment vehicle. TYPES OF REAL ESTATE INVESTMENTS While there are numerous ways to invest in real estate, we’re going to focus on three primary ways average investors earn money through real estate. We touched on several of these already in the previous section. 1. Remodel and Resell HGTV has countless “reality” shows featuring property flippers who make this investment strategy look easy. Commonly referred to as a “Fix and Flip,” investors purchase a property with the intention of remodeling it in a short period of time, with the hope of selling it quickly for a profit. This is a higher-risk tactic, and one for which many of the real estate “gurus” we talked about earlier claim to have the magic formula. They promise huge profits in a short amount of time. But investors need to understand the risks involved, and be prepared financially to cover additional expenses that may arise. Luckily, an experienced real estate agent can help you identify properties that may be good candidates for this type of investment strategy… and help you avoid some of the pitfalls that could derail your plans. 2. Traditional Rental One of the more conservative choices for investing in real estate is to purchase a rental property. The appeal of a rental property is that you can generate cash flow to cover the expenses, while taking advantage of the property’s long-term appreciation in value, and the tax benefits of investing in real estate. It’s a win-win, and a great way for first-time investors to get started. And according to the U.S. Bureau of Labor Statistics, rents for primary residences have increased 21.9 percent between 2007 and 2015 as demand for rental units continues to grow.1 3. Short-term Rental With the huge movement toward a “sharing economy,” platforms that facilitate short-term rentals, like Airbnb and HomeAway, are booming. Their popularity has spurred a growing trend toward dual-purpose vacation homes, which owners use themselves part of the year, and rent out the remainder of the time. There are also a growing number of investors purchasing single-family homes for the sole purpose of leasing them on these sites. Short-term rentals offer several benefits over traditional rentals, which many investors find attractive, including flexibility and higher profit margins. However, the most profitable properties are strategically located near popular tourist destinations. You’ll need an experienced real estate professional to help you identify the right property if you want to be successful in this highly-competitive market. DOES REAL ESTATE INVESTING SOUND TOO GOOD TO BE TRUE? We’ve all heard stories, or maybe even know someone, who struck it rich with a well-timed real estate purchase. However, just like any investment strategy, a high potential for earnings often goes hand-in-hand with an increase in risk. Still, there’s substantial evidence that a well-executed real estate investment can be one of the best choices for your money. Purchasing a home to remodel and resell can be highly profitable, as long as you have a trusted team in place to complete the remodel quickly and within budget … and the financial means to carry the property for a few extra months if delays occur. Or, if you buy a house for appreciation and cash flow, you can ride through the market ups and downs without stress because you know your property value is bound to increase over time, and your expenses are covered by your rental income. In either scenario, make sure you’re working with a real estate agent who has knowledge of the investment market and can guide you through the process. While no investment is without risk, a conservative and well-planned investment in real estate can supplement your income and set you up for future financial security. If you are considering an investment in real estate, please contact us to set up a free consultation. We have experience working with all types of investors and can help you determine the best strategy to meet your investment goals. Sources: Bureau of Labor Statistics Consumer Expenditure Survey Annual Report – https://www.bls.gov/opub/reports/consumer-expenditures/2015/home.htm S&P Dow Jones Indices Press Release –https://www.spice-indices.com/idpfiles/spice-assets/resources/public/documents/574349_cshomeprice-release-0829.pdf?force_download=true Durden, T. (2016 November 29). US Home Prices Rise Above July 2006 Levels, Hit New Record High [blog post] ZeroHedge –http://www.zerohedge.com/news/2016-11-29/us-home-prices-rise-above-july-2006-levels-hit-new-record-high

Categories

Recent Posts